I think that how one lives is more important

than how long one lives.

So I don't feel too bad.

Lim Yoon-taek (32 Year old South Korean cancer victim)

Pro-Liberty Thought of the Day

Best Mockery of the Day

[From Porter Stansberry: Editor's note: we believe the issues in today's essay are so important, we're making an exception to our usual policy of vigorously enforcing our copyright.] I've abridged and made minor wording and other edits below...

A Letter from the Chairman of Government Motors

Dear shareholders,

Moody's Investors Service last week upgraded General Motors' rating. Nobody was more surprised than me.... all of the other major ratings houses (S&P, Fitch, Egan Jones) continue to rate our corporate obligations as "junk" – speculative debts that have a significant risk of default.

I'm the chairman of a publicly owned corporation, whose debts are soaring, whose margins are collapsing, and whose capital structure is still controlled by the government and our unions. So when the reporters called me to ask about the Moody's upgrade, I said: "Good things happen when you build great cars and trucks and deliver strong financial results." [Notice I didn't say "we did"...] In the first six months of 2012, we generated $2.8 billion in automotive operating profits. In the first six months of this year, we made a little more than $2.1 billion. Thus, our core, global automotive business has seen its operating profits decline substantially… by more than 24%.

We are approaching another crisis at GM, one that has its roots in the bailout of 2008/2009. The faulty bankruptcy process caused this crisis by failing to address our largest obligations (pensions and retired employee health care). At GM, we abandoned capitalism in 2010 when we emerged from bankruptcy. Instead of treating all of our creditors fairly, we gave the lion's share of the company's assets to the federal government and the UAW health care trust. Meanwhile, we didn't do anything to mitigate our enormous pension liability, which today stands at $26 billion. At the end of the bankruptcy process, none of our 400,000 retired workers lost a nickel. On the other hand, our shareholders, creditors, and many of our suppliers were wiped out.

In total, we've made about $26 billion in operating cash flow – what our main business generated before paying capital expenses and similar costs – since we emerged from bankruptcy .So where did this money – the so-called free cash flow – go? In total, we've sent around $18 billion in cash to these interests – far more than we've been able to earn. These payments started with $3.9 billion in dividends on special "preferred" shares the union, the U.S. Treasury, and the Canadian government got during the bankruptcy process. Another $8.5 billion went to repay debts to the U.S. Treasury and the union, obligations that we were saddled with in bankruptcy. But in this case, the $5.1 billion worth of stock we bought back ALL came from the U.S. Treasury. We paid a $2-per-share premium to the actual market price of our stock. It was the U.S. Treasury stealing $400 million from the shareholders. So we continue to owe far more to unions and governments than we're earning. In addition to about $8.8 billion in cash payments we made to support our pension plan and other retirement benefits, we contributed in 2011 60 million shares of stock (worth $2 billion) to the pension plan. In 2012, we announced a big deal to eliminate our entire legacy, white-collar-salary pension obligations. We paid the Prudential insurance firm around $3.5 billion to manage $25 billion worth of our pension liabilities, taking them off our books.

In the three years after bankruptcy, we made roughly $6 billion-$7 billion in "free cash flow." Somehow, that cash was supposed to cover $18 billion in obligations. And for our common shareholders, our real owners? We haven't paid a cent. To pay off the union then, we'll have to borrow money… billions. In the first six months of 2012, we sold $74.5 billion worth of cars around the world (automotive revenues). We made an operating profit of $2.8 billion, a margin of merely 3.8%. If anything were to happen to consumer demand, these puny margins would disappear overnight.

We can't compete on price because we don't have the cheapest costs. Instead, we have the highest. GM will have to compete on credit. We'll have to work out a deal with Wall Street to borrow billions and billions and funnel the money to car buyers who the other makers won't lend to...You might recall that our company's last foray into finance didn't end well… huge losses at our former finance subsidiary were one of the primary reasons our company spiraled into bankruptcy back in 2008. Our loan book has ballooned to $11.5 billion. We made about 75% of these loans to borrowers with FICO scores lower than 600. Unbelievably, we're even lending billions (more than $3 billion, actually) to folks with FICO scores less than 540.

I call it morally corrupt crony unionist/government strip mining, a dying cash cow... This has all the stink of the city of Detroit issuing debt under circumstances of inadequate disclosure to gullible bondholders, issuing debt they knew they would never be able to pay off under a collapsing tax regime for stop-gap coverage of pensions. If you can manage margins only in the range of artificially low long-term Treasury rates after years of pent-up auto demand, how are you ever going to clear yourself of debt and unfunded liabilities, never mind invest in innovative products and infrastructure? But depending on high-risk borrowers to sell cars smells like the subprime mortgage crisis redux....

There is no way GM survives another recession; GM's only real shot was for the unions to share the pain as well as bondholders and stockholders. Obama didn't "save" the auto industry--he fought to save crony unionists, whose unsustainable contracts largely contributed to GM's problems as it shed lower-margin product lines; if foreign producers could profit in abandoned segments, they certainly could compete in higher margin segments. Checkmate! Game over! There will be no second federal bailout with a GOP-controlled House, and any future attempt to manipulate future bankruptcies will result in Obama's impeachment.

Personally I think China is biding its time; GM is a favorite brand in China. I would not be surprised to see China attempt a buyout. I seriously doubt, given Obama's attempt to describe the auto industry as an American "crown jewel", that Obama and a bipartisan group of protectionist legislators would would allow that to happen. I think it's more likely China would buy a large stake in the company and/or offer to buy GM operations in China. This is sheer speculation, of course.

I hold no position (including any short position) in GM. But the single best thing GM could hope for (beyond necessary union givebacks and improved cash flow) is getting the US government to relinquish all remaining equity in GM, something I called for some time back.

There is no way GM survives another recession; GM's only real shot was for the unions to share the pain as well as bondholders and stockholders. Obama didn't "save" the auto industry--he fought to save crony unionists, whose unsustainable contracts largely contributed to GM's problems as it shed lower-margin product lines; if foreign producers could profit in abandoned segments, they certainly could compete in higher margin segments. Checkmate! Game over! There will be no second federal bailout with a GOP-controlled House, and any future attempt to manipulate future bankruptcies will result in Obama's impeachment.

Personally I think China is biding its time; GM is a favorite brand in China. I would not be surprised to see China attempt a buyout. I seriously doubt, given Obama's attempt to describe the auto industry as an American "crown jewel", that Obama and a bipartisan group of protectionist legislators would would allow that to happen. I think it's more likely China would buy a large stake in the company and/or offer to buy GM operations in China. This is sheer speculation, of course.

I hold no position (including any short position) in GM. But the single best thing GM could hope for (beyond necessary union givebacks and improved cash flow) is getting the US government to relinquish all remaining equity in GM, something I called for some time back.

The Best President of the Past Half-Century

|

| Courtesy of the Libertarian Republic |

Two things are clear:

- Obama and the Democrats think that they will politically benefit from any shutdown and furthermore benefit from the GOP's internal conflict

- The Republicans will be portrayed as the loser by the mainstream media.

Consider one absurd Democratic talking point--the 2011 S&P downgrade of its US credit rating was "caused" by the GOP wanting a leaner budget. True, S&P was concerned about the budgetary uncertainty caused by divided government, but there were 2 sides to the dispute, and credit rating agencies are concerned with the ability to pay off new debt; that is affected by factors like the aggregate debt and loan terms, i.e., interest rates. The fact that the government has to borrow hundreds of billions just to pay its current expenses, including about $300B in interest on the debt, is not favorable. True, this year the deficit is likely to be under $1T (probably somewhere between $600-700B) for the first time in Obama's Presidency, but the projections I've seen show the debt spreading, not thinning, in future years. Here is the salient point:

The outlook on the long-term rating is negative. We could lower the long-term rating to 'AA' within the next two years if we see that less reduction in spending than agreed to, higher interest rates, or new fiscal pressures during the period result in a higher general government debt trajectory than we currently assume in our base case.To analytically-challenged "progressives", S&P wants less spending--less need for new debt, less risk of the need to raise interest rates to attract buyers of new debt, fewer budgetary constraints if ObamaCare costs surpass projections, not to mention the risk of a recession which could shrink revenues and raise safety net costs. The S&P is apolitical; it's not going to point its finger at Obama's intransigence on Keynesian spending sprees and failure to compromise or back his own deficit reduction commission's proposals, but clearly the focal point of any dispute has to be the President.

I kept a low profile on Cruz' quixotic filibuster in an attempt to defund ObamaCare. The problem is, everybody knows the government is going to be funded; conservatives want their priority, defense spending, to be funded, and nobody wants to see the global markets roiled over a shutdown. If I had a vote, I would have voted with the 19 behind the defund effort but more saliently against the unconscionable budget, But I can understand why one of my favorites, Tom Coburn, wasn't one of the 19: you shouldn't throw out the baby with the bathwater; ObamaCare is hardly the biggest line item in the budget, and Coburn, who was part of the bipartisan majority in Simpson-Bowles, probably is worried about picking one's battles and thinks this plays into Democratic propagandists' hands.

As I write, I've seen email notifications that the House has sent another bill to the Senate, this one postponing the individual ObamaCare individual mandate and the medical device funding surtax, but an emboldened Majority Leader Reid and Barry Obama have already said no deal. This one I think will get more Senate GOP support. I think Reid and Obama are on much thinner ground here, because there is a clear double standard. Obama will not enforce the employer mandate--something not even allowed under his own law. I think, once again, this is mostly a political maneuver to force vulnerable Democrats in next year'selection to vote on the record.

Eventually, I think Obama gets what he wants, although Speaker Boehner is suggesting a shutdown is in play if the Senate turns the new proposal down. However, Obama should be careful of what he wishes for--his personal approval rating according to Gallup is at 43 and a net disapproval of 7 points. ObamaCare is also an unpopular policy. If there is a shutdown or if the markets are roiled, Obama will take a hit. Does he really want to argue why giving individuals the same year's grace he is giving business is worthy of shutting down the government over? Of course, if the House folds, it will lose a lot of credibility. But they do not fear a President with a 43% rating; even if Obama wins, he loses. The Dems think the Republicans are trapped, but Obama is not the Clinton whom survived the 1990's shutdown.. In this case, the Dems may win a Pyrrhic victory: the President will be weakened, and the Senate will likely be lost next fall. Obama should sign onto the new House bill; I think the political costs outweigh the benefits. It may well be that Obama falls into Boehner's trap by rejecting the bill.

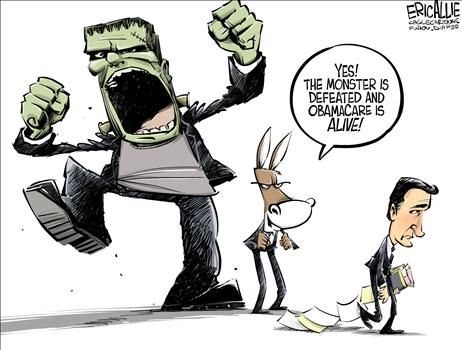

Political Cartoon

ObamaCare can only survive by the lifeblood of subsidies, much more than the Democrats' disingenuous kaleidoscope accounting estimates. Even Dracula couldn't survive without a more robust economy. Cruz was not likely to win over both the Democratic Senate and President.

|

| Courtesy of Eric Allie and Townhall |

The Supremes, "I Hear a Symphony"