For I am a Bear of Very Little Brain,

and big words Bother me.

Winnie the Pooh

Chart of the Day

|

| Courtesy of the Gray Lady via Tucker |

The services that are rising the fastest in price are those most afflicted by government intervention and control: college, health care, (overregulated) child care. Every single good or service that has fallen in price and thereby become more available is mostly or entirely a product of free-market production and distribution. And remember that this has happened despite the attempt by the Federal Reserve to increase prices on everything.Image of the Day

|

| Via Drudge Report |

Still More on Piketty

In recent posts, I've discussed the best-selling French socialist Politics of Envy tome, reflecting on reviews by Austrian School economist Bob Murphy and free-market economist Don Boudreaux. This commentary reflects a 4-part series by Austrian School economist Randall Holcombe for the Independent Institute. (The fourth post has not been published as of this date.)

In Holcombe's first post, he gives an overview of the book, which does a comprehensive review of economic history of income inequality across countries and that has increased over the past 3 decades. (Piketty essentially argues that this unsustainable trend will inevitably trigger social unrest and prescribes a wealth tax to mitigate unrest.) Holcombe takes issue with Piketty's conceptual framework for extrapolating the trend over the coming decades: "His framework misrepresents the nature of capital, how it is valued, and how owners of capital earn their returns." Capital is not some intrinsically return-yielding simplistic conceptual blob; it must be productively deployed to earn a return. Piketty does play lip service to this distinction, but this nuance is not reflected in his empirical framework.

In his second post: "Piketty says “the first fundamental law of capitalism” is that the share of income going to capital, α, is equal to the return on capital, r, times the capital/income ratio, β, or in equation form, α=rxβ." Holcombe has two issues here: (1) the dubious measurement of β as an aggregate monetary value, and (2) he argues Piketty's equation has it absolutely backwards, i.e., β=α/r. Think, for instance, of a bankrupt company: regardless of what shareholders invested in the company, the company has not generated a return: the worth of their investment is zero Holcombe uses Piketty's example of a 1-million euro Paris apartment that reaps 30,000 euros in rent. If r=4%, Piketty argues that an increase in rent to 40,000 euros is inevitable. Nonsense, Holcombe replies: the value of the apartment is only as good as its market-clearing rent. If indeed r=4%, the market value of the apartment is really only 30000/.04=750,000 euros. Holcombe ends his essay with this seminal insight: "Piketty laments the increase in inequality since 1980, but setting aside inequality for the moment, anyone who has lived in a capitalist economy since that time can see the increase in the standard of living that everybody — not just the economic elite — has enjoyed. That increase in the general standard of living has been due to the employment of capital in productive uses by its owners, but this economic function of the owners of capital plays no role in Piketty’s analysis."

In his third post, Holcombe further reflects on his transformed version of Piketty's equation, this time reflecting on values of r. As anyone knowledgeable of basic arithmetic knows, holding α steady, β increases as r decreases, and β decreases as r increases. Consider how r is impacted by interest rates. In general, we would pay more for a bond as the risk decreases: for example, there is no meaningful risk that the federal government will default on its notes, so we are willing to pay more for the bond. On the other hand, if a company or local/state government runs into revenue/cash flow problems; bondholders would bid the price of the bond security down to reflect the increased risk they're taking. Second, let's consider the effects of monetary policy. As the Fed manipulates interest rates downward to near-zero, this suggests that r decreases, which suggests that the market is willing to pay more for an asset. (HINT: what does this suggest happens to stock and bond prices if and when the Fed raises interest rates?) Why is an Austrian School economist pointing this out in response to Piketty? Note that Austrian School economists despise activist monetary policy; they tend to believe this stimulates artificial bubbles and inevitable busts. Holcombe is basically arguing that the inequity that Piketty has observed is largely an artifact of loose monetary policy and it's gone about as far as it can go, because you can't push nominal rates below zero. In essence, the trend behind Piketty's observed trend over the past 3 decades is temporary/unsustainable and is not an artifact of capitalism but rather of dysfunctional government policy.

Facebook Corner

|

| Via IPI |

The resident troll also is looking at only part of the state resident tax burden. According to the Tax Foundation, in 2010 (note: before the tax hikes) only 2 states west of NY had state/local tax burdens exceeding 11%, the other being the People's Republic of California. If the troll was a legitimate businessman, he would know the government cost burden must be taken into account when it comes to establishing or expanding local operations. Texas, on the other hand, was one of a handful of states with a cumulative tax burden under 8%. Checkmate, tax-and-spender.

If Illinois was sitting on oil it would be the same story. A vast sum of jobs in Texas are low skilled minimum wage earned jobs. And that is only happening because the cost of living is so low. Throw in a several months of cold weather and it would be the same as here. States are going to continue to cut each other's throats with tax rebates, no taxes. That worked for the NFL for a few years.

The troll also is neglecting to point out that per capita income in Illinois has dropped from rank #12 in 2007 to #16 in 2012 while Texas has been a stable #25 and closing the income gap. Texas has a diversified economy with about 16% based on the energy sector. It leads the nation in production of cattle and cotton, is a major producer of fruits and lumber and has the largest farming acreage in the nation. It is a major trade hub (exporting more than California and New York combined) and has several deepwater ports. It is home to 51 of the Fortune 500, including 6 of the top 50.

(IPI). Property tax hike for pensions? Chicago voters say, "No can do."

Why should today's taxpayers bail out decades of failed union-supported political leadership which made the corrupt bargain for and paid lip service to unsustainable pension plans but did not "invest" the city's fair share? Taxpayers have been paying their fair share all along through already high property taxes; pensioners and future retirees need to adjust to the reality of what has been actually invested on their behalf and not expect taxpayers, many if not most whom don't have any pension plan of their own and need to fund their own retirement, to make up the difference.

(Cato Institute). "The federal Highway Trust Fund is expected to run out of money in a few months, and unless Congress replenishes it, state highway projects will supposedly grind to a halt."

It is unconscionable that a regressive fuel tax is used as a political slush fund to fund boondoggles and money-losing mass transit. It's time we move to more of a mileage-based/user fee system and privatize operations.

More Creative Proposals

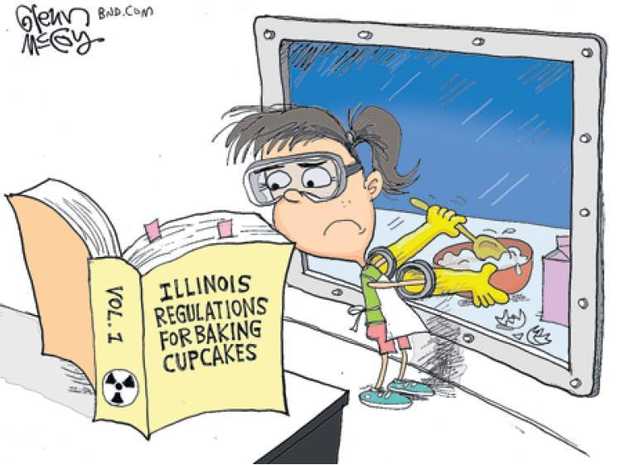

Political Cartoon

|

| Courtesy of Glenn McCoy via IPI |

ABBA, "Knowing Me, Knowing You"