The difference between stupidity and genius is that genius has its limits.

Albert Einstein

Image of the Day

I Know It's Past Christmas, But I Just Stumbled Across This Magnificent Performance

Daughter of American Idol Contestant Will Melt Your Heart

More Economic Ruminations

I am not a betting man, but I think the steep oil price drop is close to a bottom. In part, you have to look at the spread between supply and demand, which is not that large. We know from the law of supply and demand that a drop in price should increase the demand, if for no other reason that oil-importing nations are seeing prices they haven't seen in 4 years and know that there's never been a better time to replenish their reserves. Not to mention that the supply has to decrease because much supply is in unconventional, expensive to recover oil, uneconomic at current prices--and many oil producers are in volatile regions of the world and any regional tensions threatening major exporters could reverse prices in a heartbeat. Still, I have to acknowledge there is some potential downside and buyers may be waiting to see prices stabilize. The problem is that markets rarely sound trumpets at market bottoms.

What's surprising to me a bit is the strong dollar bubble. In part, this is an artifact of major economic issues in Japan and Europe, where bond yields are even cheaper than the ultra-safe US Treasury "gold standard" (meaning not the yellow medal, but a baseline in an uncertain world)--why would you settle for half of the interest of a European bond, when the European debt situation is worse than ours?) If indeed there are deflationary pressures, getting a 1.8% interest rate might not be so bad...

I personally think, though, that we can't sustain a peak exchange rate indefinitely. In part, it reflects that the market is anticipating the Fed raising rates. I'll believe it when I see it; keep in mind one or 2 positive quarters does not signify a robust economy; the energy sector has taken a huge hit, the economy seems to be picking up more part-time vs. full-time positions, and incomes have barely improved; if we had a more robust economy, we should see incomes climbing with employers competing for workers. A lot of share price growth reflects stock buybacks vs. organic business growth. We aren't seeing job-yielding capital investment increasing despite more stable balance sheets. The reason I mention all this is that I think if and when the Fed has raised rates, it is flirting with recession (increased business costs, lower profitability). Not only that but higher American rates could trigger doom for emerging market debt, and make American exports much more expensive to the rest of the world. With the Fed already falling short of inflation goals, the impact of higher interest in national debt service, Obama appointing another inflation dove to the Fed Reserve, I just don't buy that the Fed will raise rates anytime soon. Sooner or later, it will act to counter "beggar thy neighbor" currency wars. Not to mention that Yellen, a monetary dove, is hardly one to push interest rate increases; I guarantee she's far more concerned about the deflation bugaboo.

One of the reasons I've been expounding all this is that if and when the Fed makes its intentions clear, we could see commodity prices firm up and/or recover to an extent that inflation is not reflected in rates. An old tried and true tactic to counter foreign devaluations is to flood the market with dollars, e.g., asset purchases, better known as QE.

A final note. A financial writer I've usually respected basically ridiculed the concept of the Fed setting artificially low rates and essentially revisiting the savings glut vs. central bank intervention debate. The savings glut theory basically argues that declining interest rates reflect too much money chasing too few securities: a simple matter of supply and demand. The Austrians argue that low interest rates shift towards a more immediate consumption perspective (because savers lose purchasing power) and businesses have more incentive to take on higher-risk, longer-term investments (e.g., research and development). Why an outflow and/or excess savings rates in developing countries? In part, the overconsumption in Western countries could only be sustained by foreign producers; these developing markets yielded a surplus of savings from exports feeding the developed market consumer boom with an inadequate consumer economy and a shortage of domestic consumption/investment alternatives. The Austrians argue a market interest rate would moderate consumption to a more sustainable level and provide more of an incentive to lower order production; developing nations would need to develop their economies given lower consumption from developed countries.

As you can tell, I'm more sympathetic to an Austrian perspective. There is no doubt that central bankers are manipulating the system; for example, just the knowledge that the Fed is going to buy bonds is going to support bond prices. No bank is going to get into a pricing war with the Fed over securities. There's no doubt that pegged currency rates can be maintained by purchases/sales of related securities. But the real cause of the distorted economy is a fundamental disconnect between production and consumption. Low rates change incentives for both production and consumption; a free market alleviates these distortions.

Facebook Corner

(Fox Business). A growing number of cities are banning sledding. Judge Andrew Napolitano says individuals need to push government to stop prohibiting potentially dangerous activities: "People [should] rise up and say, 'Let my kid sled down that hill...'"

This is an unsustainable game of Whac-a-Mole. What are you going to do next--ban skiing because someone might break a leg or run into a tree? Interesting topic, though, because my maternal uncle as a boy once went sledding down the street of my grandfather's house (a steep drop downhill), the sled overturned, a blade gashing my uncle badly. (And my uncle, a retired priest, personally said to me that his mother said a prayer over him and the bleeding stopped.) I don't recall my uncle calling for a ban on sledding after his accident. There are all sorts of risks in life; for example, air and bus travel are far safer than ordinarily driving; should we ban driving? We need to engage in serious tort reform, capping damages and sanctioning lawsuit abuse.

(National Review). Talk of an “Obama boom” is premature.

Unfortunately, Capretta goes off the track, especially towards the end of the essay. The question of federal austerity and economic growth is hardly as decided as he implies--which I consider an unnecessary concession to the Keynesian political religion. Consider the fact that the highest rates of economic growth in US history were achieved with a small federal government, and there are several examples of sharply declining spending (e.g., after the World Wars) where the economy quickly rebounded after short recessions/depressions. Of course, as Murphy points out in a mises.org piece, Krugman engages in all sorts of Keynesian apologetics to explain away at least 9 major examples where spending cuts were followed by stronger economic growth.

Yes, if you accept the traditional definition of GDP where government spending is considered strictly additive, cutting spending would be seen as a negative for the economy. But this is a methodological problem. Spending is an offset to revenues--which are offsets from the real (private) economy, and those effects, as Bastiat reminds us, involve those who, if not having their property unduly stolen by Statists, would otherwise save, invest or consume--certainly far more efficiently and effectively than government monopolies.

Spending cuts can be made intelligently vs. the "progressive"-preferred economically-damaging alternative of increased plunder to support bloated spending. For example, many government watchdog groups have outlined ways of reducing spending through operations reengineering and streamlining, greater resource sharing, more open marketplaces of human capital, etc. Arguing that cutting wasteful spending as in mothballed Pentagon failed projects, etc. is "harmful" to the economy is patently absurd--a modern-day retelling of the broken window fallacy. Maybe overpaid bureaucrats and contractors benefit from government boondoggles, but that's like pouring water into a leaky bucket: we would be better off simply paying off the parasites and cancelling huge overhead costs.

Now would a GOP Administration simply engage in Keynesianism Lite as the author suggests? Not necessarily; consider the historical reality of Harding-Coolidge, who sharply cut spending in the aftermath of WWI. I do agree that G.W. Bush was no fiscal conservative, given sharply higher domestic spending in his first term, an unpaid-off Medicare drug benefit, a stimulus handout early in the Great Recession, and, of course, TARP. One can make the argument with the possible exception of Reagan there have been no real GOP fiscal hawks nominated to the Presidency since Coolidge (maybe Goldwater). What would a real fiscal hawk do? I submit the exact opposite of the Obama regime--they would have done everything to reduce regime uncertainty, downsize the tax and regulatory burden, restore rule-based monetary policy/sound money, open up free markets and trade, engage in meaningful reform of unsustainable entitlements, etc.

(Lawrence Reed). Tonight for the first time, I watched this 2005 film [Joyeux Noel] about the amazing Christmas truce of 1914. Yes, it was a reminder of what a senseless, unnecessary and ghastly error World War I was, but it was also a moving tribute to the decency in the human spirit. It will bring tears to your eyes, guaranteed. I highly recommend it and would like to ask the Facebook friend who brought it to my attention last month to contact me so I can send a token of gratitude. In his review of the film, the late Roger Ebert wrote, "Its sentimentality is muted by the thought that this moment of peace actually did take place, among men who were punished for it, and who mostly died soon enough afterward. But on one Christmas, they were able to express what has been called, perhaps too optimistically, the brotherhood of man."

I think I saw it first on Netflix and was so blown away I immediately ordered a DVD copy.... Great movie.

(Ron Paul). Here’s my take on auditing the Fed: An important step. http://bit.ly/1w6uBrR

Not just audit but strip away the second mandate, the full employment mandate, which is like a blank check for activist monetary policy...

(National Review). Anyone remember the Fugitive Slave Act?

Anyone who looks at the 111th Congress and doesn't realize immediately it was by far the most dysfunctional over the past generation is in a state of denial and an economic illiterate. The one thing we know about sausage making in Washington: when a bunch of political whores ever agree on anything, it is either totally meaningless (like 'I love Moms, babies, and puppy dogs' act) or harmful to the free markets.

(IPI). Members of the Illinois General Assembly are among the highest-paid state legislators in the country. Only California, Michigan, New York and Pennsylvania pay their legislators higher base salaries.

Let's peg political whore income to bond ratings, labor force participation rate, and improvements in basic educational scores.

(IPI). Underground dining is an attractive option for entrepreneurs who want the flexibility to do what they love without the commitment of running a restaurant full time. But Chicago is trying to put an end to it.

Do you really want to eat somewhere that the health department doesn't do regular inspections or has a food handlers license?

Fascist OP's should keep their ignorance to themselves. It's anti-competitive propaganda as usual. Restaurants thrive on repeat business; if and when there are issues, it's usually indicative of poor management and unprofessional staff, and if you get a reputation for serving tainted food, you'll probably have a hard time rebuilding your business and reputation. It's almost impossible for a business operating unsafely to go unnoticed--employees, patrons, restaurant review bloggers, etc. I certainly wouldn't feel safer just because some corrupt health inspector did an inspection 2 weeks ago; as they say in the financial services industry, past performance is not indicative of future results.

In short, fascist OP trolls have more faith in the credibility of government bureaucrats who can't even boil an egg than someone whose business lives or dies on each day's transactions. Who is more motivated to worry about safety--some public parasite who has a job regardless of the accuracy of his inspections, or the business owner who can get sued for serving unsafe food?

I Love Black Labs...

Last year, as the faithful reader knows, I had a thing for traditional wedding proposals, and I embedded many of them. (I may check for fresher clips in the weeks ahead.) My latest thing is watching new puppy clips; I myself don't own a dog mostly because of my frequent road warrior status over the years and the hassle of finding apartments allowing pets. This clip caught my attention for obvious reasons. The familiar reader may recall my fondness for black labs; a few years back, while I lived in Maryland, for about a week, I came home from work at night and as I walked to my locked building entrance, I was startled by a beautiful, friendly, sweet jet black lab emerging out of the dark brushing her body against my left shin; I found it endearing although I had never met the dog before. The funny thing was when I first opened the building door, she surged past me, scampered down the steps and parked herself right in front of my own apartment door, looking up at me as if to say, "What's taking you so long, slowpoke?" (I diverted her attention to get into my apartment without her.) She greeted me like that for a solid week, no matter when I got home. It got me speculating whether I should "adopt" her (even though I've never bought an ounce of dog food) when all of a sudden the mysterious affectionate greetings stopped.

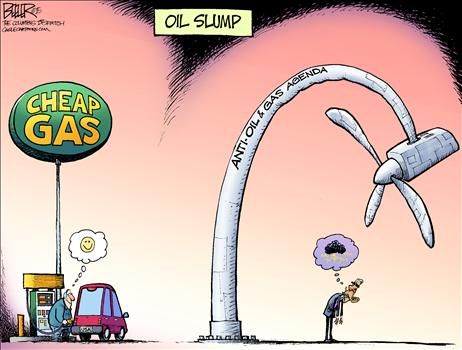

Political Cartoon

|

| Courtesy of Nate Beeler via Townhall |

Glen Campbell, "I'm Not Gonna Miss You". This marks the end of my Glen Campbell retrospective; I love, love, love this performance, Glenn's last (forced by his advancing Alzheimer's, the story behind this song), and I don't care who else wins, but I strongly want to see him take home the prize for at least one or hopefully both Grammy nominations. My next series will feature Céline Dion.